Chapter 71 11/06 USDX: It's Yet Too Early to Predict Another Sharp Decline in the USD

Summary: The October US employment figures fell significantly below the 12-month average monthly growth rate of 258,000 jobs. It's a mixed report that confirms the slowdown in the US economy is sufficient to justify pausing rate hikes but doesn't signal an imminent recession. Therefore, it's premature to anticipate another substantial decline in the US dollar at this point.

Fundamentals

The US Dollar Index declined for the third consecutive trading day on Monday as market participants continued to digest the lower-than-expected October nonfarm payrolls report.

The report from the US Department of Labor last Friday revealed that the US labor market added 150,000 jobs in October, below the expected 180,000. While the labor force participation rate declined from 62.8% to 62.7%, the unemployment rate unexpectedly increased from 3.8% to 3.9%. Wage growth also slowed from 4.3% to 4.1%, its lowest point in two years.

For the market, this report appears to strike a balance, confirming that the US economic slowdown justifies the Federal Open Market Committee's (FOMC) decision to pause rate hikes while not signaling an impending economic recession. However, it is still a relatively weak report that underscores the message the market received from last week's FOMC meeting, suggesting that the Fed's rate-hiking cycle appears to be "done." We expect that the Fed will not cut rates before the fourth quarter of 2024, but if the economy weakens further before then, a rate cut might come earlier.

In terms of the market, this report is a perfect combination of short-term risk relief. The labor market continues to create employment opportunities at a healthy economic pace. Meanwhile, wage growth is slowing down rather than accelerating. The rise in the unemployment rate reflects an increased interest in finding new employment.

This combination reinforces the expectation that inflation is moving towards normalization, and central banks won't need to tighten policy further. It's a matter of waiting for the effects of the implemented rate hikes rather than aggressively tapping the monetary tightening pedal.

On Friday, the US Dollar Index fell to its lowest level in six weeks. Now, the market sees a reduced likelihood of further rate hikes in December, which is unfavorable for the US dollar. We believe that Friday's significant decline suggests a shift to a more classical correction pattern. It's too early to anticipate another substantial decline in the US dollar, as the state of the US economic activity hasn't deteriorated to a sufficient extent.

This week, the market will be listening to speeches from Fed Chairman Powell and many other members at the International Monetary Fund (IMF) meeting. Increased risk sentiment, along with the ten-year US Treasury yields, may provide some trading opportunities for a moderate slowdown in the index.

Technical Analysis

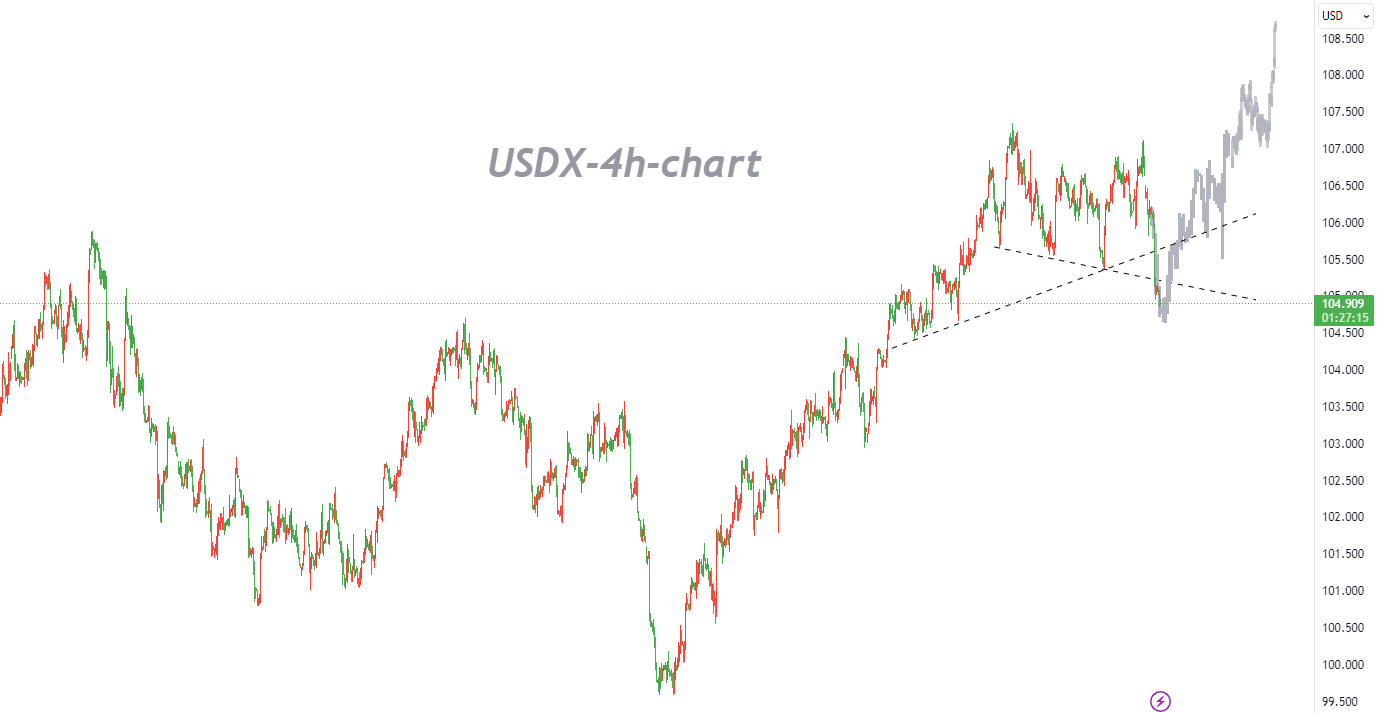

The US Dollar Index hit a six-week low last Friday, and its continued decline on Monday aligns with established expectations.

Nevertheless, the USD bulls still maintain a constructive outlook and are likely to regain an upward momentum before entering a bearish phase. This is because the overall uptrend remains intact, and the expectation of a significant upward trend continuation persists following the consolidation phase.

After a corrective phase, the bulls are now expected to break through the critical resistance level at 105.25 and test the second resistance at 105.73. Breaking through the latter would sustain the high-level consolidation pattern.

On the other hand, any new weakness is likely to find support around the 104.42 level. Failure to do so could open the door to a deeper correction or lead the asset into a bearish territory initiated by a double-top pattern.

Lastly, the fundamentals are also favoring the US dollar, as the US economy maintains resilience and outperforms other major economies (EU, China, and Japan). This will help the Fed maintain higher interest rates for a longer period than other major central banks. Additionally, escalating geopolitical tensions exacerbate risk aversion sentiment, further supporting the safe-haven US dollar. In terms of trading, a buy-on-dips approach is recommended.

Trading Recommendations

Trading Direction: Long

Entry Price: 105.00

Target Price: 108.75

Stop Loss: 104.00

Valid Until: 2023-11-20 23:55:00

Support: 105.14, 104.86, 104.69, 104.42

Resistance: 106.76, 107.03, 107.88, 108.79